Announcement on the Investigation and Handling of Abnormal BTC Futures Liquidation Orders

Dear Valued Users

At 20:17:14 on July 31, 2018, one abnormal overloss order occurred on the BTC0928 futures: 4,168,515 futures cont were sold to close long, resulting in huge overloss losses and potentially a large overloss ratio. Overloss rules are a fundamental component of all futures products and an issue the entire industry has been working hard to solve. OKX does not gain any earnings from overloss. A simple example is as follows: two users, A and B, each provide 1 BTC as margin. Assuming the BTC price is 1 USD and each futures has a value of 1 USD, at this price, User A opens long 10 futures with 10x leverage, and User B opens short 10 futures with 10x leverage, forming a position of 10 futures. If the spot index price drops from 1 USD to 0.1 USD, User B, who opened short, theoretically profits 9 USD, and User A loses 9 USD. However, User A's margin is 1 BTC, has a value of 1 USD, which is not enough margin. Therefore, although User B's position shows an earnings of 9 USD, due to limited margin, User B can only earnings a maximum of 1 USD, and the other 8 USD are subject to overloss. OKX has always been committed to optimizing risk control rules to reduce the probability of overloss. For example, the early overloss system, the limit price system, and after overloss is triggered, the order price of the overloss order will be placed at the marketplace price plus or minus 1%, etc. Some users with special intentions use this to attack OKX for targeted overloss. In fact, such price fluctuation in the marketplace are all caused by overloss orders.

The incident unfolded as follows: customer with USER ID 2051247 started engaging in a large number of abnormal long position-building transactions beginning at 2 AM on July 31st. Upon monitoring this abnormal behavior, OKX's risk control department immediately took measures, communicating with the customer multiple times, requesting them to reduce their position to mitigate marketplace risk. After several communications, the customer refused to cooperate, and the OKX platform then froze their account. However, due to a sharp drop in BTC price, their position was ultimately liquidated.

As stipulated in the 'OKX Virtual Futures Customer Usage Agreement':

6.2 OKX has the right to issue warnings, restrict trades, and close accounts for all malicious price manipulation, malicious influencing of the trading system, and other unethical behaviors. When necessary, OKX has the right to adopt means such as suspending trades, canceling trades, and rolling back period trades to eliminate adverse effects.

6.3 When a customer's position quantity or order quantity is excessively large, and OKX believes it may pose serious risks to the system and other customers, OKX has the right to require customers to adopt risk control measures such as canceling orders and flattening positions. When OKX deems it necessary, OKX has the right to implement for individual accounts measures such as restricting total position quantity, restricting total order quantity, restricting opening positions, canceling orders, and forced flattening for risk control.

OKX Platform Solution is as follows:

1. The OKX platform takes 2500 BTC from its own funds and injects it into the risk reserve fund pool to reduce the apportionment ratio.

2.If, during the settlement process at 4 p.m. on August 3, 2018 (this Friday), there is any manipulation of the settlement price by an account, we will delay settlement by 10 minutes, manually update the settlement price or delivery price to a reasonable value before proceeding with delivery settlement, and freeze the trading and withdrawal of the manipulating account.

Following this incident, the OKX platform will upgrade its risk control measures to prevent similar issues from recurring. The specific optimization plan is as follows:

1. "Anti-Manipulation Strategy" will be active on August 4 (development is nearing completion).

Plan: For 'cross margin mode', the larger the position, the more margin required, to maximize the cost of malicious manipulation; for 'isolated margin mode', a limit will be set on the number of open positions to reduce the marketplace risk that large positions might cause. Specific details are as follows:

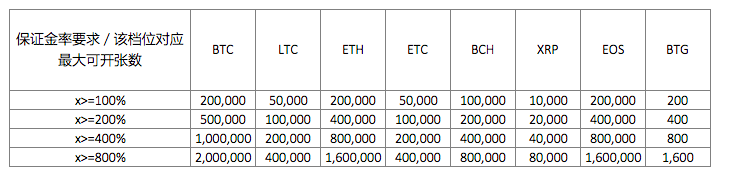

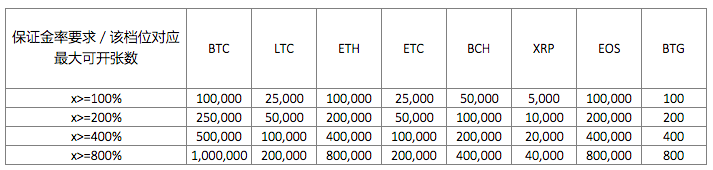

Cross Margin Mode:

10x Leverage:

20x leverage:

Isolated Margin Mode:

Maximum open positions limit for 10x leverage:

Maximum tradable quantity limit for 20x leverage:

In addition, for clarity, the margin level calculation formula will also be revised this time, removing the concept of adjustment coefficients.

The original formula is as follows:

Cross: Margin Ratio = Account Equity / (Margin required for customer's position + Margin frozen for pending orders) - Adjustment Factor

When the leverage is 10x, the adjustment coefficient is 10%; when the leverage is 20x, the adjustment coefficient is 20%; when the margin level is less than or equal to 0, the customer's position will trigger liquidation.

Isolated Margin: Margin Level = (fixed margin + unrealized PnL) * average entry price * leverage / (contract size * position quantity) - adjustment factor

When the leverage is 10x, the adjustment coefficient is 10%; when the leverage is 20x, the adjustment coefficient is 20%; when the margin level is less than or equal to 0, the customer's position will trigger liquidation.

The new formula is as follows:

Cross margin: margin ratio = account equity / (margin required for the customer's position + frozen margin for open orders),

Isolated margin: margin level = (fixed margin + unrealized P&L) * average entry price * leverage / (contract size * position quantity)

After the adjustment of the aforementioned new formula, the forced liquidation logic is adjusted to: at 10x leverage, when the margin level is less than or equal to 10%, the customer's position triggers forced liquidation; at 20x leverage, when the margin level is less than or equal to 20%, the customer's position triggers forced liquidation.

The above logic is merely an adjustment of concepts, and the timing of triggering liquidation has not actually changed. This formula change will become active along with the anti-manipulation strategy.

2. 'Mark price' active at the end of August (in smartling glossary test)

The plan is to use the mark price to calculate customers' unrealized profit and loss, margin level, and other metrics. Forced liquidation will only be executed when the mark price reaches the estimated liquidation price.

Mark price algorithm: Spot index price + EMA (futures marketplace price - Spot index price)

The principle is to use the spot index price plus a reasonable recent basis as the fair price of the futures market. This fair price, because it uses the EMA algorithm and considers the basis for a period of time, means that even if abnormal users use large funds to manipulate the futures market price, it cannot cause the mark price to change rapidly in a short period of time, thereby reducing the probability and risk of users being liquidated due to abnormal manipulation.

3. 'Mechanism for setting different risk limits based on position size' and 'liquidation process optimization' to become active in September. (Development started on August 7th)

Solution:

a) Set different risk limit mechanisms according to position size

Customers' positions are classified. When the position is larger, the margin required to maintain the position is higher, thereby ensuring that the position has more margin for effective flattening, minimizing the risk of overloss.

b) Liquidation Process Optimization:

When a customer's position faces liquidation risk, the system will automatically attempt to reduce the customer's position to lower MMR, thereby maximally preventing the liquidation of the customer's entire position.

Position Reduction Process (Example):

Assume a customer holds 100,000 cont and is at position level 3, with a maintenance margin ratio of 2.5%. If the maximum holding for level 2 is 80,000 cont, with a maintenance margin ratio of 2%, the system will automatically reduce their position by 20,000 cont to lower the maintenance margin ratio requirement for the customer's position and prevent the remaining position from being liquidated. If the maintenance margin ratio requirement for level 2 is still not met after the reduction, the reduction will continue until the lowest level is reached.

4. 9Risk Reserve Deduction Optimization will go active in September (development started in mid-August)

Solution:

a) When unfillable liquidation orders incur losses up to a certain percentage, the current maximum loss will be immediately deducted from the Risk Reserve Fund.

b) Re-place the order at the best available price in the current marketplace, to fill as quickly as possible and reduce further overloss.

c) When the risk reserve fund is insufficient, a unified allocation will be made on Friday.

The above scheme can cap the maximum overloss when an overloss position occurs, preventing further expansion of overloss during delivery and settlement.

We will spare no effort to accelerate futures optimization, making the platform's risk control mechanism increasingly perfect, and we also welcome our valued customers to provide us with more suggestions: futures@OKX.com.